DOI: 10.18441/ibam.26.2026.91.227-251

Julián Bilmes

Instituto de Investigaciones en Humanidades y Ciencias Sociales, Universidad Nacional de La Plata / Consejo Nacional de Investigaciones Científicas y Técnicas, Argentina

jbilmes@fahce.unlp.edu.ar

ORCID ID: https://orcid.org/0000-0003-1170-1526

Rodrigo Kataishi

Instituto de Desarrollo Económico e Innovación, Universidad Nacional de Tierra del Fuego, Antártida e Islas del Atlántico Sur / Consejo Nacional de Investigaciones Científicas y Técnicas, Argentina

rkataishi@untdf.edu.ar

ORCID ID: https://orcid.org/0000-0002-6316-1528

Cao Ting

Center for Latin American Studies, Fudan University, Shanghai, China

caoting@fudan.edu.cn

ORCID ID: https://orcid.org/0000-0003-2189-7024

The relations between the People’s Republic of China (PRC) and Latin America and the Caribbean (LAC) have been increasing considerably in this Century. Energy, food and raw materials represent the main economic interest of PRC in the region, based on its outstanding endowments in those areas and the Chinese needs for its food, energy, supply, industrial and technological security. It has been suggested that, after the first “raw materials boom” (or commodity Supercycle) of the period 2002-2013 in Latin America, due to massive Chinese demand in products like oil, copper, soybean and bovine meat, nowadays we would be witnessing the emergence of a new boom between China and Latin America, this time based on Chinese demand of critical minerals for energy transition (González Jáuregui 2024, 3).

The topic of critical minerals has assumed an increasingly important role on the global agenda. These are elements such as lithium, copper, graphite, nickel, cobalt and rare earth elements, which are key to energy transition technologies towards clean and renewable sources, as well as to techno-economic competition and war industries. As the International Energy Agency (IEA) shows, a typical electric car requires six times more mineral inputs than a conventional car, and an onshore wind power plant requires nine times more mineral resources than a gas-fired power plant, while, since 2010, the average amount of minerals required for a new unit of power generation capacity has increased by 50% as the share of renewables in the global energy matrix has grown (IEA 2021).

Lithium, usually called “white gold” in the media, is conceived here as a “star mineral” for the energy transition global agenda due to its uses for the emerging green economy, especially in batteries: both for electronic devices and electric vehicles, the latter being one of the fastest growing and most globally competitive areas in recent years. This mineral has motivated an intense bilateral interest, investments and cooperation agreements along the last decade, given the outstanding endowments of resources and reserves in the “Lithium Triangle” compounded by salt flats in Bolivia’s west, Chile’s north and Argentina’s northwest. The focus of this article is put on the Argentine case, which appears in second place at world level in terms of resources, third in reserves and fourth in production, with the biggest quantity of production projects (50 currently, in different stages of development, MECON 2024a). Given the profuse literature existing about these topics, we center the analysis on a series of cooperation agreements signed between Argentine and Chinese actors, being one of the main topics of bilateral interest in the last decade.

The objective of this article is to analyze the China-Argentina cooperation on lithium, paying attention to the opportunities that arise for the development strategies raised by both countries regarding the value chain of this natural resource. So, we seek to characterize what type of cooperation is established, considering investments and financing characteristics, for one side, and if the several bilateral agreements signed in the last years imply technology transfer, innovation and/or local techno-productive capabilities scalation. A qualitative methodological strategy was adopted, which implied gathering, survey, systematization and analysis of information, by using reports and databases of public and private entities, newspapers and energy and mining media, together with the review of specialized literature on the subject.

The approach is based on Latin American and heterodox political economics articulated with a geopolitics perspective. From that viewpoint, the article adopts the notion of strategic natural resources (SNRs) as a conceptual lens to understand the geopolitical and developmental relevance of lithium. SNR are those natural endowments whose control, transformation and circulation are central to national security, industrial policy and the global distribution of technological and economic power. Their significance derives from their material properties –such as finite availability, high economic value and essential uses in key technologies– as well as from their embeddedness in state strategies, market dynamics and territorial conflicts. SNRs are thus a category at the intersection of political economy, resource governance and global competition over technological futures. In Latin American debates, this approach has been developed by authors such as Fornillo (2021) and Svampa (2019), who emphasize how resources like lithium concentrate rents, power, and developmental dilemmas. Recent contributions have reinforced this view, showing how minerals essential to the energy transition are increasingly subject to securitization, industrial policy planning and geopolitical contestation (Bian et al. 2024; Bilmes et al. 2025).

The article is organized as follows. In the first section after this introduction, we present a brief overview of the development path of each nation, the strengthening of their relationship and some theoretical insights to precise our approach. In the second section, the geopolitics of critical minerals and their close connection with the energy transition agenda is presented, as well as the relevant role of Latin America and Argentina as providers of this SNR for the global economy and the PRC. In the third section the focus is put on the characteristics of the lithium value chain, the prominent position that the PRC has achieved on it and particularly in Argentina, considering trade, investments and participation in lithium projects. In the fourth section we present several cooperation agreements that took place in the last years between governments and companies from both countries, analyzing the main aspects, implications and obstacles of this bilateral cooperation. Finally, the conclusions end up with an articulated analysis of the relevance, perspectives and risks of the lithium boom and Argentina-China cooperation on this matter.

Contemporary China is conceived as the most important and successful case of autonomous development by a peripheral nation in the world. Its development path reflects a sovereign project with national particularities since its 1949 social and national revolution, which has undergone the most accelerated process of growth, urbanization and industrialization in history over the last four decades, combining a strong process of industrial and technological development with political and strategic autonomy (Rosales 2020; Merino et al. 2024). This path was unfolded first under a conception of strong centralized planning and pretensions of autarchy during the Maoist stage, and then under a conception of openness and liberalization since 1978, while preserving the state direction of economic development out of the hands of capitalists (Gabriele and Jabbour 2022). The Chinese impressive economic, social, educational and health achievements, among other issues, are particularly exceptional for being the most populated country in the world (until 2023, when it was surpassed by India), with an enormous territorial extension. Until the beginning of xix Century, China represented a third part of the world economy, as the historical center of Asia, but the Western powers defeated and subordinated it, entering a period known as the “century of humiliation” (1839-1949). Since the revolution, the country started a process of reconstruction of national power and wealth, and in the last decades the PRC has become the great industrial workshop of the world and the main trade power, achieving dispute in this xxi Century both the economic and techno-productive leadership and the reconfiguration of the world order. In this transition, it can be observed a jump from semi-periphery to economic center in its more developed centers (its big coastal cities) and from regional power to great world power.

Argentina, on the other hand, being a middle-income and peripheral country with a big territory and relatively small population, has been marked by a historical “pendulum” of competing political projects and their respective development models. If by the beginning of 20th Century, the Latin American country celebrated its Centenary as a nation under the imaginary of “world’s breadbasket” because of its agro-export model, between the 1940s and 1970s became an emerging industrial power and reached half of China’s GDP by the 1960s-1970s. Both economies occupied a semi-peripheral position during this period and were industrial and technological leaders in different sectors –however, despite Argentina, China was already one of the five main power poles–. Nevertheless, Argentina entered a process of peripheral decline, deindustrialization and loss of state and techno-productive capacities from the 1976 civil-military dictatorship until 2001. Then, a neo-developmentalist process was deployed between 2002 and 2015, and to a lesser extent, between 2019 and 2023, after the return of peripheral neoliberalism, a model deployed between 2015 and 2019, and again since 2023. In this itinerary, the country has not managed to recover a consistent development path, being trapped in recurrent economic, political and social crises (Merino and Haro Sly 2023). Beyond this convulsed and unstable trajectory, natural resources have occupied a privileged place on the Argentine development path, especially for its lands (the richness of the humid pampas), and others have been added in recent years to the main visions of development in the country, on the basis of the potential of its energetic resources and minerals, existing several social and political struggles about its usufruct and rents (Cantamutto and Schorr 2022).

The PRC and Argentina have had diplomatic relations since 1972, and from the end of the past century they started a process of strengthening their relationship by signing numerous bilateral agreements on investment and trade. Already in the new century, and within the Chinese Going Out policy, the two countries signed a Strategic Partnership in 2004, followed in subsequent years by other instruments as the Strategic Dialogue for Economic Cooperation and Coordination, in 2010, and the scaling of the bilateral association with the sign of a Comprehensive Strategic Partnership in 2014. More recently, Argentina entered Chinese-based international initiatives as the Asian Infrastructure Investment Bank, in 2020, and the Belt & Road Initiative, in 2022, with the occasion of the Year of Friendship and Cooperation China-Argentina (due to the 50° anniversary of the establishment of formal diplomatic ties). Additionally, for the impetus of Brazil and China, the country was invited in 2023 to join the expanded BRICS+ forum, although, finally, the current Argentine government that assumed in December 2023 refused to accept this invitation (Vaca Narvaja 2024).

Along this process of strengthening of the bilateral relation, the trade between Argentina and China increased from two billion dollars by 2000 to more than twenty-five in 2023, that is, multiplied 15 times, which led PRC to become the second trade partner of the former (ECLAC 2023). Moreover, China played a key role for the Argentine economy in the last years as destiny for its exports, main financier of great energy and transport infrastructure projects and the expansion of the Central Bank’s reserves (through the swap mechanism). In this framework, PRC have represented for Argentina both an important partner in economic, political and even diplomatic terms (considering the Malvinas Issue and One-China principle, or joint positions in terms of democratization of world financial order) as well as a risk of reprimarization and deindustrialization, because of its huge demand of Argentine raw materials and the supply of cheap industrial products. Different types of cooperation agreements and strategic projects have been developed in areas like Sci-Tech, modernization of railway lines, construction of nuclear and hydroelectric power plants, wind and solar parks, with very different models from the Argentine side due to factors such as governmental policy changes, macroeconomic crises and the socio-state capacities available to the country in each sector of activity (Andrés 2023; Bilmes 2025).

As it is stressed by Kataishi and Cuntin (2023), China appears as a negotiator partner to Argentina, more than an economic competitor, although huge scale disparities between them exist. They recommend observing key criteria to analyze the bilateral agreements, considering mutual benefit of strategies, previous specialization patterns and potential niches, existing potential complementarities between both economies. However, an important obstacle for Argentina is that, in contrast to China, it has not been able to align and coordinate State strategies in the mid-term, with financial and business sectors to operate in a joint form to concrete strategic investments.

It is relevant to recover here, briefly, some debates that take place in the specialized literature. For some scholars, China recreates in Latin America the process of dependency, positioning most countries as suppliers of natural resources in the global value chains controlled by the Asian giant, while the region maintains its historic extractivist character1 and peripheral insertion in the world economy (Svampa 2019; Stallings 2020). For others, the rise of China, within the broader reemergence of Eurasian nations and multipolar scenario, implies a questioning of the Western-based world system and its logic of uneven and combined development of the process of accumulation of wealth and power (Merino et al. 2024). In this sense, the PRC does not have an imperialist or “Western” pattern of development, whereby the processes of accumulation are guaranteed and reinforced by political and military force (Katz 2024).

So, far from narratives either of demonization or idealization of China –i.e. seen as a menace or a salvation for LAC nations–, it is understood here to be more useful to recover the idea of a “hybrid geoeconomics” of the PRC in the region. According to Salgado Rodrigues (2020), this implies a paradoxical cooperation and manifest itself in the duality between the immediate economic benefits –mainly in commerce, investment and loans– and, on the other hand, in the neglect of challenges for medium-long term development, minimizing the perception of domestic vulnerabilities and the generation of an asymmetric and dependent relationship. However, there is no presence of ideological imposition and/or economic conditions on China’s part, but only and exclusively prerogatives based on the Chinese economic-political development itself. If such a link with China is pursued, there are certain economic risks of deepening a primary export profile without added value at origin, deindustrialization and loss of economic complexity for LAC productive matrices, given the huge scale and techno-productive disparities.

Notwithstanding, at the same time, China appears as a strategic partner with great potential to overcome this peripheral, “underdeveloped” and dependent condition of LAC nations, given that its rise –along with reemergent Eurasian powers and the Global South– challenges the modern world system and its associated logics: the center-periphery structure, the interstate hierarchies and international labor division (Merino et al. 2024). Also, the Chinese South-South development cooperation covers new practices of political dialogue, trade agreements and infrastructure financing, rooting –in discourse, at least– in the “Bandung spirit” of Non-Aligned Movement (Vadell et al., 2020). To overcome this kind of paradox, as reading here, in line with Fernández et al. (2023), it appears necessary to define an autonomous project and development strategy from Latin America and Argentina, strengthening regional integration, deploying strategic vision and planning, structural capacities, sovereign control of power levers, and social and popular rooting. This constitutes a key current challenge.

In this framework, we would like to know what kind of possibilities, opportunities and contradictions arise for Argentina in the context of China’s rise on the world power map. In this sense, we wonder whether, in the face of this bilateral relationship, Argentina adopts a project of autonomous development that does not lose sight of national sovereignty and endogenous state and techno-productive capacities, as China itself has adopted in its international relations.

As Siroit (2024) points out, commodities critical to the world’s largest economies have been recorded, classified and analyzed for decades. However, it is only in recent years that the current critical minerals (CM) framework has taken shape, with resources listings being updated almost automatically in response to advances in industry and technology. According to the IEA, at least 35 countries around the world have adopted 450 CM policies, and 100 of these have been introduced since 2020 (Johnson et al. 2024). The latest version of the U.S. listing includes some 50 minerals, and in its 2023 update an additional listing for the energy sector was incorporated. Other major players, such as the European Union and Japan, have their own listings, with 34 and 32 minerals, respectively, while China’s is the shortest, with 28 minerals, of which 16 are rare earths (Siroit 2024).

The rise of the CM framework is explained, firstly, by the growing demand for these SNR as the global agenda of energy transition to clean and renewable sources advances, because of the harmful effects of climate change and the dangers that this implies for the sustainability of life on the planet. This boom has also generated great volatility in the prices of CM (with exponential increases and some dizzying declines, especially in the case of lithium), together with the appearance of bottlenecks in supply chains and the associated growing geopolitical disputes. In fact, there is growing concern in the geopolitical West about the vertiginous rise of China, which appears to be a major contender in this geoeconomic struggle, as can be observed in several reports from think tanks warning about the backwardness of the US and its allies in the technological competition (Merino et al. 2024). Indeed, the bid for CM is also part of the competition to lead the new techno-productive paradigm on the rise, usually called “Fourth Industrial Revolution” or “Industry 4.0”. This new paradigm has been defined as a convergence of physical, digital and biological technologies, referring to a process of automation and digitalization of production processes. Indeed, this techno-productive revolution is triggering energy consumption, especially electricity, a key input for digital technologies (being artificial intelligence its core) and which should be generated based on clean and renewable sources, according to the energy transition agenda. In this framework, the technologies of renewable energy imply an exponential demand for CM. These factors help explain how lithium has become embedded in a global logic of hegemonic transition and strategic rivalry over the material foundations of the energy and digital economies.

The PRC has assumed a prominent control over the value chains of these key resources, especially regarding the refining or processing of a significant portion of CM, such as rare earths, manganese, graphite, nickel, silicon, cobalt, aluminum, indium and lithium (Bian et al. 2024). For this it depends on the import of concentrates and raw materials, so the security of supply of CM is also a major concern for the Eastern power. This has led to an acceleration of Chinese investment in the mining sector, both internally and externally. For example, Chinese investment in the metals and mining sector linked to the Belt and Road Initiative (BRI, a sort of territorial interconnection plan based in Eurasia and with a planetary projection) reached its highest level in 2023 in its entire first decade of existence, at around 19.4 billion dollars, an increase of 160% over the previous year (IEA 2024). The focus of investment and mine acquisitions abroad was on battery metals such as lithium, nickel and cobalt.

The intensification of resource extraction under the paradigm of energy transition has given rise to what scholars defined as green extractivism (Dunlap et al., 2024), a model that evidences traditional patterns of dispossession and environmental degradation on underdeveloped countries, in combination with a green narrative. This perspective highlights how large-scale, capital-intensive projects oriented to SNR (such as lithium, copper or rare earths, often located in peripheral regions), sustain unequal value capture, increasing territorial asymmetries. In LAC, critical voices emphasize how green extractivism risks entrenching dependency and ecological sacrifice zones, absent autonomous development frameworks and energy justice principles (Svampa 2019; Gudynas 2022). Rather than a structural transformation, it may signal a new cycle of accumulation built on foreign resources and environmental sacrifice.

In this framework, Latin America represents one of the most important territories in this global dispute over the access and supply of CM, given the region’s enormous wealth of SNR. In the last years, it has been clear the geopolitical struggle over these coveted natural goods, with high level declarations, proliferation of initiatives on supply security and pressures of all types from Western actors against several cooperation mechanisms deployed between LAC states and companies with Chinese private and public counterparts (Rahman and Lazarus 2023; Bilmes et al. 2025).

As Cao et al. (2020) point out, since 2012 Latin America has continuously enhanced its position in China’s diplomatic outlook. The item “Energy and resources” has appeared both as one of the six areas of cooperation priorities of the framework of pragmatic China-Latin America cooperation, known as “1+3+6”, that Xi Jinping proposed during his visit to the region in 2014, and figured as one of the ten areas of the Joint Action Plan for Cooperation in Key Areas China-CELAC (2022-2024). Nevertheless, China’s investment in LAC has bet on transcending this to encompass more diversified ways of production, cooperation and exchange, in ambits like high education, culture, tourism, sports and science and technology. In 2018, the Latin American countries were invited to integrate the BRI as a “natural extension” of the 21st Century Maritime Silk Road.

Argentina has a great mining potential, with a lower grade of exploitation if it is compared with its neighbors Chile and Peru, two of the biggest minerals producers, with whom it shares the Andean Mountains. Although mining has been a minor activity in its history, since the end of the past century it began to be strongly powered, being copper, gold, silver and lithium the most relevant minerals (in economic terms), while other minerals, such as potassium, iron, uranium, boron, molybdenum, vanadium and zinc, could have opportunities for development (Bustelo and Rubiolo 2023).

The presence of PRC in Argentina has acquired a great relevance in the last years, scaling since the 50% stake bought of “Veladero” mine (San Juan province, of ore and silver) by Shandong Gold, in 2017, for USD 960 million. According to official data (Secretaría de Minería 2023), since 2020, China appears as the second country in importance in terms of investment announcements, after Canada, reaching more than US$ 3 billion. Chinese mining companies, such as Hanaq, Shandong, MCC and CAM, have a strong presence in Argentina, in projects and investments covering a wide range of minerals in several provinces of the country. From Jujuy to Chubut, these initiatives include the extraction of lithium, gold, silver, copper, zinc, iron and lead, positioning China as a key player in the Argentine mining sector. Chinese investment in the country grew rapidly in the last decade, because of the strengthening of the bilateral relationship, while Argentina has become the third main receiver of Chinese outward foreign direct investment in LAC, after Brazil and Peru, with almost 24 billion dollars (Dussel Peters 2024). As Treacy (2023) notes, 58% of Chinese investment announced in 2000-2020 was destined to mining.

In successive editions of China Mining Fair in the last decade, Argentine mining authorities have promoted the country’s big potential, have meetings with major Chinese mining companies and signed certain cooperation agreements, such as the one over geology and mining in 2019. Then, in the framework of the Argentine entry to BRI, in 2022, it was signed a cooperation agreement for creating a China-Argentina Geoscience Cooperation Center, based on the joint work of the geological services of each country and with particular interest on lithium. In general terms, it can be observed the prominent role that energy and natural resources occupy within the main bilateral instruments, considering secondary cooperation agreements and infrastructure projects included in the financing portfolios, such as wind farms, hydroelectric dams, nuclear plants, photovoltaic plants, electric transmission lines and pipelines, and lithium salt lakes (Mantilla 2023; Bilmes 2025).

All this is highlighted by former Argentine Ambassador in China, Sabino Vaca Narvaja (2024), as the way of guaranteeing the needed financing of strategic infrastructure works in the country, especially in some of the main vectors of growth in this Century, such as green development and new energies. In this sense, the South American nation presented twenty projects of renewable energy with Chinese funding into the Green Belt & Road and the Global Civilization Initiative. In effect, in front of the global agenda of energy transition and on the base of its great potential in different types and sources of clean energy, Argentina has seen China as a key ally for this mission (Cao et al. 2023).

In this sense, in 2023, along with the signing of the Cooperation Plan for Argentine entry to BRI and several high-level visits to China which included meetings with the main Chinese mining companies, a commitment was expressed to boost Argentine lithium’s great potential. On the official mission of the then Argentine Minister of Science and Technology in China, a Memorandum of Understanding (MoU) of Sci-Tech cooperation on natural resources and energy transition was signed, and it was agreed to promote Chinese investment in the industrialization of Argentine lithium for the automotive industry. At the same time, with the aim of accelerating the trade relationship and eliminating intermediation, it was announced the opening of direct trade between the two countries through RMB, and –not casually– the first operation of direct investment through the Chinese currency in the country took place, by the Bank of China and for boosting the Chinese mining business, especially on lithium (Glezer 2023).

In short, the resurgence of state-led initiatives around lithium has prompted renewed debates on resource nationalism, industrial policy and the developmental state (Johnson et al. 2024; Obaya et al. 2021). While many Latin American countries have implemented measures aimed at retaining a greater share of resource rents and promoting domestic value addition, the effectiveness of these strategies remains uneven. In Argentina, the coexistence of a liberal mining framework and provincial control over subsoil resources has generated fragmented governance, limited policy coordination and weak enforcement capacity (Juste and Rubiolo 2023). Moreover, the turnkey nature of many cooperation projects with Chinese firms –characterized by bundled financing, engineering, and equipment provision– tends to reinforce technological dependence rather than foster autonomous development (Treacy 2023; Bustelo and Rubiolo 2023). This tension between extraction and transformation lies at the core of Argentina’s lithium dilemma: whether to remain a raw material exporter or to build the institutional and industrial capacities necessary to move up the value chain.

Lithium is the lightest metal and the lowest density solid element, making it a good conductor of heat and electricity. These characteristics make it possible for lithium batteries to store a greater amount of energy in a relatively small and light system, which, added to the fact that they have the highest charge/weight ratio (key for means of transportation), has made them the market’s favorite battery (COCHILCO 2023). Thus, it is a key component for the energy transition because lithium batteries and accumulators are essential for storing the energy produced by renewable sources and supplying it to the electric devices or vehicles that use them. In addition to its potential for reserving high energy densities in small batteries, its fast charge and the possibility of recharging without reaching zero give lithium an advantage compared to cobalt, nickel, copper and rare earth elements. This is why it appears as the CM with the highest growth projection (IEA 2024).2

The uses of lithium are diverse: stationary batteries, electromobility, electronics, lubricating greases, medicines, glass and ceramics, polymers, air conditioning, metallurgy, among others. Until a decade ago, these uses were more diversified, but over the years, batteries are the item that concentrates the bulk of their applications: if by 2012 they represented 29%, by 2020 it already exceeded 70%. The boom in electromobility plays a key role in this, since, as shown by COCHILCO (2023), 65% of the demand for this resource is used for the manufacture of electric vehicles (EV). In turn, it is estimated that in EVs the cost of batteries may represent about half of the total costs.

While the major companies involved in the lithium extraction stages are from Australia, USA, Canada and the PRC, Asian countries, mainly China, Japan and South Korea, are the main players in the more advanced stages of the chain. Emulating the renowned idea of the Latin American Lithium Triangle, where 53% of global lithium resources and 46% of reserves are estimated to be located, González Jáuregui (2024) postulates an Asian Battery Triangle, given that around 87% of lithium demand is concentrated in that continent, particularly in three countries: China (55%), South Korea (20%) and Japan (12%), which are the main possessors of technologies for lithium-ion batteries (LIB) production.

PRC is the country that has achieved the most in advancing vertical integration. Its companies have acquired a leading role in the global value chain of this coveted mineral, both in terms of production and processing (like Tianqi and Ganfeng) and LIB manufacturing and EV production (like CATL and BYD, respectively). A wide range of Chinese companies control around 60/70% of world lithium refining, specializing in battery production, especially in the most knowledge-intensive segments such as the production of composites and batteries. In this sense, China appears today as the main world producer of cathodes (between 70 and 80%, according to different estimates), electrolytes (75%), anodes (90%) and cells (80%), among other elements that compose them, largely dominating the value chain of these batteries3 (Bian et al. 2024). This dominant position in this market implies both a strong Chinese influence on international prices of lithium carbonate and lithium hydroxide, and the possibility of producing at much lower costs than its competitors. In this regard, an estimate by the Oxford Institute for Energy Studies puts the cost of building a lithium refinery outside China at three to four times higher than building one inside the country (Emont 2024).

Due to its strategic importance, the territories in which lithium is found are fiercely disputed by the powers that be to gain control of it to guarantee its supply for their industries. The countries that possess lithium have adopted different strategies regarding the possession of the resource: from those that have decided to export it as compounds –either as lithium carbonate, hydroxide or chloride– to others that have promoted instruments either to capture its rent, develop local production networks and/or adding value. In fact, in recent years lithium resource nationalism has emerged through a wide range of measures (Johnson et al. 2024), either via taxation, royalties, nationalizing private firms and investments, as well as fostering forward and backward linkages or export bans without local processing, amid the rising global protectionist wave.

A large Chinese deployment can be seen in recent years. According to the IEA, between 2018 and the first half of 2021 China invested around US$4.3 billion in lithium, double what the US, Australia and Canada together invested in the same period. According to some estimates, half of that investment volume went to Latin America, with around 90% of lithium investment projects in the region coming from China (Mining Press 2023). Moreover, by 2023 it was estimated by S&P Global Ratings that half of the world’s biggest lithium mines put on the market since 2018 were bought by Chinese companies, i.e. 10 of the 20 lithium mines up for grabs, for an estimated US$ 7.9 billion (Fowler 2023).

Regarding the tightly connected item of electromobility, in 2022 it represented 35% of foreign direct investment from PRC to Latin America, in the order of US$ 2.2 billion, mostly concentrated in Brazil, Mexico and Argentina, while 70% of the EVs imported by the region and 90% of the LIBs imported by South America came from China in 2023 (The Economist 2024). In this sense, Lopes Kotz (2024) argues that, while it may be yet soon to affirm, evidence point to the articulation of a regional value chain in green technologies led by Chinese firms, with Chile and Argentina producing strategic minerals and batteries, while manufacturing capacity for EVs and solar panels is located in Brazil, which could serve as a hub for exporting to the region as a whole.

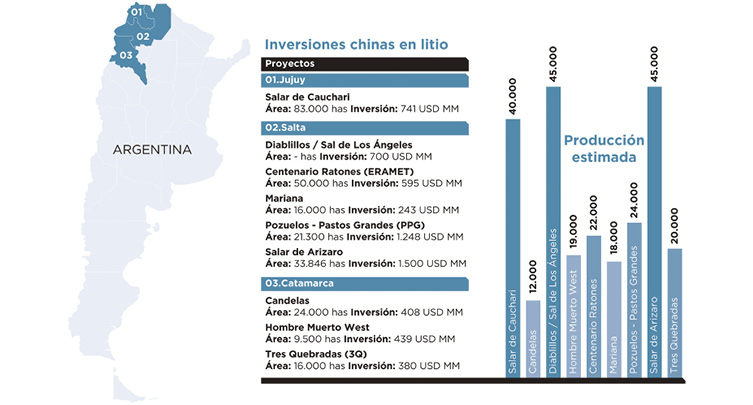

Argentina appears as the second largest holder of lithium resources in the world, with 21% of the total, and in third place in terms of reserves (i.e., technically and economically feasible resources for extraction), with 13% worldwide, according to U.S. Geological Survey data for 2024. While the country occupies the fourth place in terms of production, with around 5%, in the period 2010-2022, it was the jurisdiction that received the highest exploration budget worldwide on average, with 22%, and ranked third in 2023, with 17%. As of 2024, three projects are in commercial production, out of 50 with varying degrees of progress (MECON 2024a). In 2022, Argentina exported more than US$ 300 million in minerals to China, and above 92% of that amount corresponded to lithium carbonate, followed by silver and its concentrates. The PRC appeared as the main lithium exports destination, with almost 42% of the total (Secretaría de Minería 2023). In 2023, China accounted for over 40% of the country’s exports and invested a total of US$ 2.7bn in the lithium sector (Johnson et al. 2024).

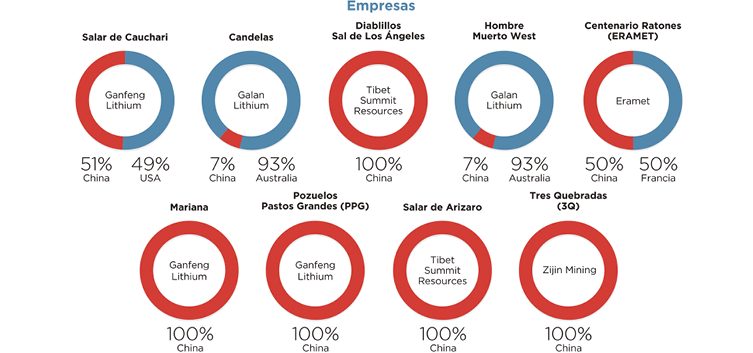

Since the end of the past century, the preeminence on this sector oversaw transnational companies from USA, Canada, Australia, Japan and South Korea, while Chinese companies expanded rapidly its positions in the last decade. Companies as Ganfeng, Tsingshan, Zijin, Zangge, Tibet Summit Resources, Hanaq and Revotech acquired an important position in the Argentine lithium sector through different measures as mergers and acquisitions, and they have participation in fourteen projects, mainly in advanced stages (i.e. with resources already identified and proven feasible for extraction, and with construction permits for the project already approved, or construction already underway). In the following figure it can be observed the Chinese participation within the most important projects.

According to González Jáuregui (2024), Chinese companies present peculiarities compared with the other enterprises: their interest in Argentine lithium is not limited to a financial business neither profitability in short or medium term, but they point to control lithium carbonate battery-grade that the plants will produce, in order to export it to China and use it there for fabrication of batteries and other related products.

In contrast to other types of managing the local tensions generated by this “lithium fever” in the Northwest of the country, Chinese companies (as well as Canadian ones) have signed agreements with affected indigenous communities in the territories where each project is placed. These agreements imply investments and donations for building or repairing schools, libraries, community centers, providing internet access and PCs, job provision, training and monetary compensation (González Jáuregui 2021). In effect, this is a sensitive problem for all types of extractive projects, given the relevant anti-extractivist movement and social opposition to them throughout the country, due to the lack or deficiencies of environmental impacts studies; free, prior and informed consent processes and public controls to extractive projects.

The previous overview of Chinese participation in the Argentine lithium sector is accompanied here with a detailed analysis of the profuse cooperation agreements carried out by governments, State agencies and companies of each country in the last lustrum. In first place, a Table is presented hereinafter, with the details of several exchanges that have taken place since 2021.

Year | Issue | Parties involved | Planned investment (if applies) |

2021 | MoU for producing urban EV and lithium batteries in Jujuy province | Argentine Gov. – Jiangsu Jiankang Automobile (PRC) | Not informed |

2021 | MoU to set up a lithium battery factory in Perico (Jujuy) and promote the use of EV | Argentine and Jujuy Gov. – Ganfeng Lithium (PRC) | Not informed |

2021 | Agreement to advance negotiations to associate YPF Litio with CATL to jointly develop lithium battery production projects | Argentine Gov. – YPF (Arg.) – Contemporary Amperex Technology Company (PRC) | Not informed |

2022 | Agreements to set up a battery cells plant for electro-mobility in Perico (Jujuy) | Jujuy province Gov. (Arg.) – Gotion High Tech (PRC) – JEMSE (Jujuy company) | Not informed |

2022 | Agreement to set up joint factories: one for cells and batteries in Jujuy and other for EV in Venado Tuerto (Santa Fe province) | Argentine Gov. – Gotion High Tech (PRC) – Iraola Group (Arg.) | US$ 12 million (first stage) |

2022 | MoU for joint investment, exploration, exploitation, production and industrialization | YPF (Arg.) – Tianqi (PRC) | Not informed |

2022 | Cooperation agreement for industrialization lithium value chain after purchase of “Laguna Caro” project (Catamarca) | Argentine and Catamarca province Govs. – JinYuan (PRC) | Not informed |

2022 | Provision of Chinese machinery for cells and batteries factory in La Plata (UniLiB) | YPF-Tecnología (Arg.) – Xiamen Tmax Battery Equipments (PRC) | – |

2022 | Association to operate Salinas Grandes project (Salta) | CST Mining (PRC) – REMSa (Salta company) | – |

2023 | MoU for setting up a factory of hydrogen chloride and sodium hydroxide in Perico industrial park (Jujuy) destined for lithium carbonate production | Jujuy province Gov. (Arg.) – Tsinghan Mining Development (PRC) | US$ 120 millions |

2023 | Commitment to establish an EV plant in the country with batteries produced in Jujuy | Chery (PRC) – Argentine Gov. – Gotion (PRC) – JEMSE (Arg.) | US$ 400 millions |

2023 | Alleged agreement to produce batteries in Catamarca | YPF and CAMYEN (Arg.) – Zijin Mining (PRC) | – |

2023 | Alleged negotiations for battery production agreement | YPF (Arg.) – CST Mining (PRC) | – |

2023 | Inclusion of “Tres Quebradas” project (Zijin Mining) in complementary works list of bilateral Cooperation Plan for BRI | Argentine and Chinese Govs. | US$ 380 million (first stage) |

2023 | High-level meetings in China to boost and evaluate the progress of projects in Argentina | Argentine Gov. – Tibet Summit Resources, Ganfeng, Gotion, CST Mining and Tsingshan | US$ 5790 millions |

2023 | Cooperation agreement for lithium industrialization, clean extraction, production and import of minerals needed to manufacture electric batteries in Argentina. | China and Argentina science and industry authorities | – |

2023 | Inclusion of “Tres Quebradas” and “Cauchari-Olaroz” projects in List of Practical Cooperation Deliverables of the Third Belt and Road Forum for International Cooperation | China, Argentina and other countries members of BRI | – |

2024 | Agreement to train and qualify engineering students in Jujuy province | National University of Jujuy (Arg.) – Tsingshan (PRC) | – |

2024 | Agreement for development of mining, research and technological training in Catamarca province | Catamarca Gov., National University of Catamarca, Mining Suppliers and Labor Association (Arg.) – Lishang New Energy Technology, Sichuan Three-Rare Times Technology and Audes Group consortium. | – |

As can be observed in the Table, lithium and its value chain are a prominent topic in the bilateral relation in the past years, generating several types of exchanges and agreements. The first big issue to highlight is the existence of many joint projects related to industrialization of the lithium value chain through batteries and EV factories. This is important given the Argentine recent bet on generating added value, both through political and business channels: i.e., via national and provincial governments and enterprises, both public and private, national and provincial ones. However, a debate exists in the country about the national development strategy to adopt, and it is a mistake to think that simply having lithium means batteries can be manufactured (Obaya et al. 2021; Heredia 2023). Indeed, not only the proportion of this metal in the total materials of a battery is low (depending on the type of battery, it can vary between 2 and 8%, with copper, graphite, nickel, and manganese being the most used minerals), but this industry is closely linked to electromobility and the need to develop demand on a regional scale.

In second place, it can be noted high-level meetings between Argentine authorities and Chinese companies to negotiate terms, conditions and advance degree of the extractive projects and planned investments, and intergovernmental agreements which put certain Chinese lithium projects in Argentina within relevant bilateral diplomatic instruments, as those related to BRI.

Besides national government initiatives, the provinces also play an important role in this type of bilateral cooperation. In effect, northwest peripheral Argentine provinces have found in China a providing ally of financing and technology for boosting the potentialities of their territories (Juste and Rubiolo 2023; Juste 2024). In this line, their mining and energy companies (JEMSE, REMSa and CAMYEN, from Jujuy, Salta and Catamarca provinces, respectively) have a relevant paper in this process as key local partners in the associations with Chinese companies. As can be observed in the Table, especially JEMSE, and CAMYEN and REMSa to a lesser degree, had established agreements with Chinese counterparts regarding certain commitments of producing and/or industrializing lithium value chain and scaling to EV production.4

Moreover, despite the proliferation of recent cooperation agreements, they usually do not include specific clauses of technology transfer and/or joint technological and industrial development between the Chinese companies and its Argentine counterparts, be it the State, the scientific system and/or local companies (González Jáuregui 2024). This is coherent with the more general trend of many cooperative projects around renewable energy, which are carried out under a turnkey model, in which the PRC assumes financing, planning, engineering, equipment and supplies acquisition, construction and commissioning, with a linkage model that promotes the dependency to Chinese capital and companies in most cases, with none or little know how and technology transfer (Bustelo and Rubiolo 2023; Juste 2024). In this case, exceptions to this trend are the agreement of JinYuan in Catamarca province, which stipulates “technology transfer from China to Argentina” (News ArgenChina 2022), and the recent agreements of 2024 in Jujuy and Catamarca that commit to train and qualify engineering students and labor force.

Institutional fragmentation is a critical bottleneck for advancing national strategies in the lithium sector. The constitutional transfer of natural resources to the provinces –enshrined in the 1994 reform– has led to a decentralized model of resource governance, in which provincial governments negotiate directly with foreign firms. While this framework enhances local autonomy, it often undermines national coordination, dilutes bargaining power and generates regulatory asymmetries. At the same time, the absence of an integrated policy ecosystem –focused on the articulation between industrial policy, science and technology, environmental regulation, and large-scale investments– has limited the capacity of the Argentine state to steer lithium governance toward concrete actions for engaging autonomous strategies. These structural gaps expose how formal sovereignty over key resources does not necessarily translate into sovereign control over their strategic use and valorization (Fornillo 2021; Fuentes et al. 2023).

Then, certain cases of turnkey contracts to gain local capabilities exist, such as the provision of the initial equipment, machinery and supplies for the first Argentine lithium cells and batteries pilot plant (named UniLib) installation. This obeys to an association of the technological brand of the historic Argentine National Oil Company (NOC), YPF, called Y-TEC, and National University of La Plata. The purchase was guided by an international bid won by Chinese company Xiamen TMAX, which provided 70 machines from China, including mixers, ovens, cyclers, cutting/stack, dehumidifiers, and two large presses of 13,000 kilograms each (Bembi and Bilmes, 2024). The conglomerate of YPF has had an important role in this cooperation. Besides the UniLib case, it can be seen in the Table the agreements and negotiations that the company –or some of its brands– had with Chinese counterparts such as Tianqi, Zijin, CST Mining and CATL. This is due to the fact that the Argentine NOC, which was privatized in the 90’ and renationalized in 2012 (Bilmes 2023), passed in the last decade from being merely an oil and gas company to an energetic one, more broadly in line with a global trend that obeys to the energy transition agenda, and it has established technological and lithium branches (Y-TEC, with the National Council for Scientific and Technological Research, and YPF Litio, respectively) which have bet to take part in this value chain (Fuentes 2024).

Nevertheless, these domestic initiatives to add value in the lithium value chain are not articulated, given the lack of a national development strategy over this SNR. This disarticulation is due to the Argentine mining development model, which have been characterized as of “liberal orientation” (Obaya et al. 2021), or an “extractivist model” (Gómez 2023). This is due to the neoliberal structural reforms established in the 1990s and their regulatory scheme, through the Mining Investment Law and the Constitutional Reform that established the transfer of natural resources from the Nation to the Provinces. This regulatory body has enabled Argentina to be the only country in the Lithium Triangle where several private companies, many of them transnationals, are the successful bidders to explore, invest and usufruct the country’s lithium. Therefore, it presents greater advantages for foreign investments, not only because of its regulatory environment that allows it, but also because the provinces that hold the lithium resource are very prone to an economic model of concessions for transnational private investment, although with nuances among them. Furthermore, mining companies manage their own techniques and extraction processes, whose patents are instrumented in a private and confidential way, with their own R+D labs or relying on foreign universities, with whom they have long-standing cooperation traditions. Meanwhile, the country presents a disarticulation of the spheres of public policy, industry and scientific system, which makes it difficult to concrete the initiatives to add value and gain local capabilities in the lithium value chain (Fornillo and Gamba 2019).

So, as a general balance, although South-South cooperation is frequently invoked in official discourses and bilateral lithium agreements between Argentina and China, many of the mechanisms implemented continue to reproduce asymmetries analogous to those historically associated with North-South relations. In particular, the prevalence of turnkey models –in which foreign entities retain control over financing, engineering, equipment provision and construction– constraints opportunities for domestic technological learning and reinforces structural dependence. A substantive cooperative framework would require institutional arrangements explicitly oriented toward joint research and development, co-production of knowledge and sustained investment in local capacities, articulated with regional mechanisms of exchange and cooperation with neighboring countries which possess lithium or productive capabilities on electromobility. The persistent disjunction between discursive commitments and institutional design, particularly in Argentina, reveals a broader structural constraint: the difficulty of translating political convergence and diplomatic rapprochement into developmental processes capable of diversifying production structures, strengthening techno-industrial sovereignty and integrating national actors into medium and high-value segments of global value chains.

Notwithstanding, despite the precedent tensions, it is important to note this Chinese willingness to cooperate and promote joint projects as a distinct conduct, given that it is rare to find this type of agreements with other foreign companies or States, especially related to industrialization, local capabilities development and value addition. In sum, it exists certain margin of negotiation in this sense with China, unlike Western actors, but, in sum, the perspectives to effectively advance in this orientation depends on domestic factors. In fact, a big number of the agreements consigned in the Table did not reach concrete. This is a broader general problem of the Argentina-China relationship, as has been analyzed in a previous stage of this research (Bilmes 2025). In effect, considering energy and natural resources, some of the more relevant topics of this relation, it can be noted that in the last decade Chinese presence grew considerably on its own (either through mergers and acquisitions, joint ventures or biddings by its companies), while bilateral cooperation found a sort of obstacles that impeded concrete the numerous agreements signed in each area. Some explanatory factors for these obstacles have been stressed: A) Geopolitics, B) Argentine macroeconomic instability, C) Social license issue, D) Management problems.

Furthermore, the current Argentine government presided by Javier Milei has paralyzed almost all type of cooperation with the PRC, especially on strategic projects as energy and infrastructure ones. This obeys, for one side, to the cut of all the public works of that type, while it seeks to privatize as much as possible State-owned companies, economic functions and competencies, according to it “anarcho-capitalist” ideology. For the other side, the paralysis of bilateral cooperation with China keeps relation with the strong alignment of Milei’s government with the United States, especially since the assumption of the second administration of Donald Trump. Critical minerals appear as one of the main US topics of interest in Argentina, and a MoU for cooperation on this was signed between both countries in August 2024. After Milei’s victory in 2023 elections, plans to prioritize local lithium production, adding value and scaling capabilities were abandoned in favor of a strategy focused on attracting foreign investment (Johnson et al, 2024). Milei’s first major act as president was an Omnibus Law that lowered taxes, customs and export duties for international investments exceeding US$ 200 Mn, and its chapter called Regime of Incentives for Big Investments (RIGI by its Spanish acronym) allows transnational companies to take investment disputes to an international arbitration of their choice, and removes any obligation to generate employment, build local capacities or invest in technological innovation. However, from 19 investment projects in different areas presented in this Regime within its first year, the only one rejected was Mariana project, in charge of Chinese company Ganfeng Lithium (Novas and Clemente 2025).5 Finally, in this new context, although some provinces continue advancing in the bilateral cooperation with the PRC around lithium (see agreements of 2024 in the Table 1), the conditions are worse to gain local capabilities and add value in the lithium value chain –as around other SNR, in general.

Argentina appears as one of the key territories in the emerging geography of the energy transition due to the scale of its lithium endowments and the increasing relevance of this resource within global techno-industrial agendas. In this context, the growing cooperation with the People’s Republic of China has fostered a broad set of initiatives that encompass investment, scientific exchange, infrastructure and productive capacities linked to the lithium value chain. However, the extent to which this cooperation enables a shift in Argentina’s peripheral insertion remains open to question.

Although the number and scope of bilateral agreements have grown significantly –ranging from memoranda of understanding to the development of pilot plants and training schemes– their degree of implementation has been uneven, and their capacity to promote substantive transformations appears limited. Many of these initiatives continue to operate under logics that restrict local appropriation of technological and organizational know-how. In particular, the prevalence of turnkey projects and vertically integrated investment schemes by Chinese firms tends to reproduce patterns of dependence familiar from previous cycles of external insertion.

In parallel, the national governance of the sector presents notable fragmentation. The constitutional delegation of resource ownership to the provinces has contributed to the multiplication of regulatory frameworks, institutional asymmetries, and negotiation strategies that often respond to short-term dynamics and local constraints, rather than to a coordinated national project. While certain national and subnational actors have attempted to advance forms of industrialization and local linkage, these remain isolated efforts, frequently constrained by scale, institutional weakness or lack of articulation with broader policy frameworks.

From a broader perspective, the expansion of lithium extraction in Argentina echoes several of the tensions identified in the literature on green extractivism. The energy transition –while normatively oriented toward decarbonization and sustainability– does not necessarily alter the structural logics of value drain, territorial subordination and socio-environmental externalities. Rather than expressing a clear shift in development patterns, current dynamics risk consolidating a new accumulation cycle organized around critical minerals, with limited impact on the diversification of the productive matrix or the democratization of strategic decision-making processes.

Finally, the recent political and regulatory shifts introduced by the current Argentine administration have modified the horizon of possibilities for strategic planning and public stewardship of the sector. The dismantling of existing cooperation channels and the promotion of investment regimes that emphasize deregulation and capital protection over industrial or technological criteria further complicate the prospects for sovereign control of lithium. Even when cooperation with China offers potential avenues for value addition and productive upgrading, the absence of an integrated development strategy –combining industrial policy, science and technology, environmental regulation, and international engagement– remains a structural limitation.

In this scenario, the meaning and implications of the lithium boom in Argentina remain ambiguous. Far from unfolding as an automatic vector of development, it configures a contested terrain where different strategies, interests and visions of the future are in dispute. The challenge is not merely to increase investment or insertion in global value chains, but to define under what terms, with what actors, and toward which collective goals. Whether lithium becomes a platform for renewed dependency or a lever for autonomous transformation depends less on the resource itself than on the institutional and political architectures through which it is governed.

This article is result of research that has been funded with support of the Fudan Development Institute (FDDI), Fudan University, China, through FLAUC Seed Fund 2023 for two-months stay in FDDI of the first author. The research is also part of the project funded by the Social Science Research Base of the Chinese Ministry of Education for the third author, entitled ‘Study on the Change of US Diplomacy and the Competition between the US and China at the Global Level’ (No.22JJD810004).

Andrés, Mercedes, coord. 2003. Argentina-China. 50 años de relaciones diplomáticas. Cooperación, desarrollo y futuro. Fundación Germán Abdala.

Bembi, Mariela, and Julián Bilmes. 2024. “Desarrollo productivo nacional en la cadena de valor del litio: la experiencia UniLiB.” Ciencia, Tecnología y Política 7, no. 13: 125. https://doi.org/10.24215/26183188e125.

Bian, Lei, Simon Dikau, Hugh Miller, Roberta Pierfederici, Nicholas Stern, and Bob Ward. 2024. “China’s Role in Accelerating the Global Energy Transition.” London: Grantham Research Institute on Climate Change and the Environment, School of Economics and Political Science. https://www.lse.ac.uk/granthaminstitute/wp-content/uploads/2024/02/Chinas-role-in-accelerating-the-global-energy-transition-through-green-supply-chains-and-trade.pdf.

Bilmes, Julián. 2023. “Renacionalización híbrida de YPF (2012-2015): tensiones y disputas por el desarrollo y la autonomía nacional.” Cuadernos de Economía crítica 9, no. 18: 133-155.

— 2025. “Energy and Natural Resources in the Argentina-China Relationship: Interests, Cooperation and Challenges.” AUSTRAL: Brazilian Journal of Strategy & International Relations 14, no. 27: 175-210. https://seer.ufrgs.br/index.php/austral/article/view/142813

Bilmes, Julián, Pablo Fuentes, and Solange Castañeda. 2025. “El litio suramericano en la geopolítica de los minerales críticos.” En Nuestra América, Estados Unidos y China. Transición geopolítica del sistema mundial, coordinated by Gabriel Merino and Leandro Morgenfeld, 395-423. CLACSO/Batalla de Ideas.

Bustelo, Santiago, and Florencia Rubiolo. 2023. Hoja de ruta para una integración sustentable entre Argentina y China. Fundar.

Cao, Ting, Yiyang Cheng, and Longxing Wang. 2023. “Latin America’s Climate Actions and Sino-latin American Cooperation on New Energy.” (World Vision, Fudan Report Series 81, no. 4).

Cao, Ting, Yang Lyu, Xiaoyang Chen, Jin Yan & Wan’er Liu. 2020. “China-Latin America Belt and Road Cooperation: Challenges and Paths for in-depth Progress”. China International Studies 84, 107-127.

Cantamutto, Francisco, and Martín Schorr. 2022. “El carácter dependiente del capitalismo argentino y el mandato exportador.” Márgenes 8: 47-74.

Chorny, Rubén. 2022. “Litio made in Argentina. Luz verde para el oro blanco”. DangDai no. 36 (XII): 22-33. https://dangdai.com.ar/2022/10/17/dangdai-no-36-del-litio-al-auto-electrico/.

COCHILCO. 2023. El mercado de litio. Desarrollo reciente y proyecciones al 2035. Actualización a mayo 2023. Comisión Chilena del Cobre, Ministerio de Minería.

Dunlap, Alexander, Judith Verweijen, and Carlos Tornel. 2024. “The Political Ecologies of ‘Green’ Extractivism(s): An Introduction.” Journal of Political Ecology 31, no. 1: 1-28.

Dussel Peters, Enrique. 2024. China OFDI Monitor in Latin America and the Caribbean 2024. Red ALC-China. https://docs.dusselpeters.com/395.pdf.

ECLAC. 2023. International Trade Outlook for Latin America and the Caribbean, 2023. Economic Commission for Latin America and the Caribbean. https://www.cepal.org/en/publications/68664-international-trade-outlook-latin-america-and-caribbean-2023-structural-change.

Emont, Jon. 2024. “China Is Winning the Minerals War.” Wall Street Journal, May 21.

Fernández, Víctor Ramiro, Juliana González Jáuregui, and Gabriel Merino. 2023. “Latin America and China’s Belt and Road Initiative: Challenges and Proposals from a Latin American Perspective.” AUSTRAL: Brazilian Journal of Strategy & International Relations 12, no. 23. https://doi.org/10.22456/2238-6912.129527.

Fornillo, Bruno, coord. 2021. Litio en Sudamérica. Geopolítica, energía, territorios. El Colectivo.

Fornillo, Bruno, and Martina Gamba. 2019. “Industria, ciencia y política en el Triángulo del Litio.” Ciencia, Docencia y Tecnología 58: 1-38.

Fowler, Elouise. 2023. “China buys half of the lithium mines on the market.” The Australian Financial Review, August 27.

Fuentes, Pablo. 2024. “El Estado empresario en el sector del litio en Argentina: los casos de Y-TEC e YPF Litio (2013-2023).” H-industria 18, no. 35: 143-163.

Fuentes, Pablo, Julián Bilmes, and Gabriel E. Merino. 2023. “Detrás del conflicto en Jujuy: geopolítica del litio y desafíos soberanos.” Geografías desde el Sur 10. https://ri.conicet.gov.ar/handle/11336/236068.

Gabriele, Alberto, and Elias Jabbour. 2022. Socialist Economic Development in the 21st Century: A Century after the Bolshevik Revolution. Routledge.

Glezer, Luciana. 2023. “China realizó en Argentina la primera inversión 100 por ciento en yuanes”. La Política Online. 4 de septiembre. https://www.lapoliticaonline.com/energia/china-realizo-la-primera-inversion-100-en-yuanes/.

Gómez, Magalí. 2023. “Impacto de la política exterior China hacia América Latina sobre la cooperación regional: el caso del litio.” Tesis de maestría, FLACSO Argentina.

González Jáuregui, Juliana. 2021. How Argentina Pushed Chinese Investors to Help Revitalize Its Energy Grid. Carnegie Endowment for International Peace.

— 2024. “Chinese Investments in Argentina’s Lithium Sector: Economic Development Implications Amid Global Competition.” The Extractive Industries and Society 20: 101551. https://doi.org/10.1016/j.exis.2024.101551.

Gudynas, Eduardo. 2022. Extractivisms: Politics, Economy and Ecology. Fernwood Publishing.

Heredia, Fernando. 2023. “Lithium Batteries, Made in Argentina: Can They Compete Globally?” Dialogue Earth, December 6. https://dialogue.earth/en/energy/385641-lithium-batteries-made-in-argentina-can-they-compete-globally/

IEA. 2021. The Role of Critical Minerals in Clean Energy Transitions. International Energy Agency. https://www.iea.org/reports/the-role-of-critical-minerals-in-clean-energy-transitions.

— 2024. Global Critical Minerals Outlook 2024. International Energy Agency. https://www.iea.org/reports/global-critical-minerals-outlook-2024

Johnson, Craig A., Araceli Clavijo, Mauricio Lorca, and Manuel Olivera Andrade. 2024. “Bringing the State Back in the Lithium Triangle: An Institutional Analysis of Resource Nationalism in Chile, Argentina, and Bolivia.” The Extractive Industries and Society 20, 101534. https://doi.org/10.1016/j.exis.2024.101534.

Juste, Stella. 2024. “La estrategia multinivel de China y las agendas paradiplómaticas en Argentina en torno a la transición energética (2014-2023).” CONfines 20, no. 38: 43-64.

Juste, Stella, and Florencia Rubiolo. 2023. “Litio y desarrollo en Argentina: los desafíos del sistema de gobernanza multinivel y el vínculo con China.” Si Somos Americanos. Revista de Estudios Transfronterizos 23. https://doi.org/10.4067/s0719-09482023000100210.

Kataishi, Rodrigo, and Sol Cuntin. 2023. “La hegemonía emergente en clave de desarrollo periférico: un análisis en base a las relaciones comerciales entre Argentina y China durante el Siglo xxi.” I Congreso del Pensamiento Nacional Latinoamericano, 8-10 de junio, Lanús, Provincia de Buenos Aires, Argentina. https://www.unla.edu.ar/documentos/centros/manuel_ugarte/ac-tas-congreso/MESA%2020/Mesa%2020%20-%20Kataishi-Cuntin.docx.pdf.

Katz, Claudio. 2024. América Latina en la encrucijada global. Batalla de Ideas.

Lioni, Matías. 2023. “Radiografía de la inversión china en litio en el NOA argentino.” DangDai 40, no. XIII: 50-51.

Lopes Kotz, Ricardo. 2024. “China’s Green Energy Investments Aim at Latin America Amid Competition With the US.” The Diplomat, May 11.

Mantilla, Sofía. 2023. “Plan de Cooperación de la BRI”. En Cont@cto CHINA, no. 179. Observatorio China, Instituto de Estrategia Internacional, Cámara de Exportadores de la República Argentina. https://www.cera.org.ar/sites/default/files/publi-cos/2023-08/000%20En%20Contacto%20CHINA%20179.pdf.

MECON. 2024a. Litio. Argentina como jugador estratégico en el mercado global. Ministerio de Economía de la República Argentina.

— 2024b. Informes de cadenas de valor. Minería: Litio. Year 9, no. 72. Ministerio de Economía de la República Argentina.

Merino, Gabriel Esteban, and María José Haro Sly. 2023. “Argentina en el sistema mundial desde el quiebre de los 70’s a la actualidad: política exterior, proyectos en pugna y punto de bifurcación.” Relaciones Internacionales 32, no. 65. https://doi.org/10.24215/23142766e182.

Merino, Gabriel Esteban, Amanda Barrenengoa, and Julián Bilmes. 2024. China en el (des)orden mundial. La transición histórico-espacial y el nuevo momento geopolítico desde una perspectiva latinoamericana. Batalla de Ideas.

Mining Press. 2023. “China gana terreno en el Triángulo del litio.” November 2.

News ArgenChina. 2022. “La minera china JinYuan industrializará litio en Catamarca.” August 31.

Novas, Mariano, and Darío Clemente. 2025. “El RIGI en datos: balance a un año de implementada la Ley.” In El RIGI tras su primer año. El experimento libertario bajo la lupa. Observatorio RIGI, Boletín N° 1, August 2025. https://observatoriorigi.org/2025/08/16/el-rigi-en-datos-balance-a-un-ano-de-implementada-la-ley/.

Obaya, Martín, Andrés López, and Paulo Pascuini. 2021. “Curb Your Enthusiasm. Challenges to the Development of Lithium-based Linkages in Argentina.” Resources Policy 70, 101912. https://doi.org/10.1016/j.resourpol.2020.101912.

Rahman, Ali, and Leland Lazarus. 2023. “The China-West Lithium Tango in South America.” The Diplomat, October 23.

Rosales, Osvaldo. 2020. El sueño chino. Siglo XXI/CEPAL.

Salgado Rodrigues, Bernardo. 2020. “China’s Hybrid Geoeconomics in South America”. Chinese Journal of International Review, vol. 2, no. 2: 2050007. https://doi.org/10.1142/S2630531320500079.

Secretaría de Minería. 2023. Participación de capitales chinos en Argentina. Ministerio de Economía, República Argentina.

Siroit, Gastón. 2024. Los minerales críticos para las transiciones energéticas de América Latina y el Caribe. Organización Latinoamericana de Energía.

Stallings, Barbara. 2020. Dependency in the Twenty-First Century? The Political Economy of China-Latin America Relations. Cambridge University Press.

Svampa, Maristella. 2019. Neo-extractivism in Latin America: Socio-environmental Conflicts, the Territorial Turn, and New Political Narratives. Cambridge University Press.

The Economist. 2024. “Chinese Green Technologies Are Pouring into Latin America.” April 10.

Treacy, Mariano. 2023. “Cooperación y dependencia en la relación bilateral de China y Argentina: un análisis de los préstamos y las inversiones chinas en el contexto de la adhesión a la Iniciativa de la Franja y la Ruta.” Perspectivas. Revista de Ciencias Sociales 7, no. 14: 414-437.

Vaca Narvaja, Sabino. 2024. Atento al camino. Crónicas en China. Futurock.

Vadell, Javier, Giuseppe Lo Brutto, and Alexandre Cesar Cunha Leite. 2020. “The Chinese South-South Development Cooperation: An Assessment of Its Structural Transformation.” Revista Brasileira de Política Internacional 63, no. 2, e001. https://doi.org/10.1590/0034-7329202000201.

USGS. 2024. Mineral commodity summaries 2024. United States Geological Survey.

Manuscript received: 15.04.2025

Revised manuscript: 13.10.2025

Manuscript accepted: 04.11.2025

1 Extractivism is conceived as a development model based on the extraction and removal of large volumes of natural resources (such as minerals, hydrocarbons, agricultural, fishery, and forestry products), with little or no processing, and destined for export (Gudynas 2022).

2 According to the IEA (2021), global demand for lithium is projected to grow by 45% between 2020 and 2040. It should be noted that there are initiatives to advance in the commercial development of sodium-ion, potassium-ion and vanadium redox batteries for energy storage and hydrogen for electromobility that could shake the hegemony of lithium batteries in the long term. However, there are still no known materials with the energy density of lithium that are profitable in commercial terms, and battery manufacturers are already making multi-million-dollar investments in gigafactories, so the lithium battery segment seems to be consolidated, at least in the short and medium term.

3 It is estimated that, within the total cost of a battery, the cathode represents 16%, as the anode and the electrolyte 8% each (Fornillo and Gamba 2019).

4 However, as Obaya et al. (2021) have pointed out regarding JEMSE experience, its ability to invest in downstream linkages has been limited by modest resources and the small size of its production quota.

5 Up to August 2025, 19 investment projects were presented to RIGI, being mining the most important sector, with 63% of presentations, and lithium the main focus of investments, with 5 projects. While 7 projects have been already approved, included two lithium projects from British and Australian companies Rio Tinto and Galan, Ganfeng’s projects was rejected by the Evaluation Committee without providing technical specifications (Novas and Clemente 2025).